Why RTR Matters to Canadian Fintechs and Worries Traditional Banks

Real-time Rail (RTR) is about to transform the Canadian payments system by 2026, transforming the way we bank. It will facilitate instant money transfers enabling real-time payment processing making transactions faster, and more efficient.

For innovators it will open new opportunities, allowing fintech companies to develop cutting-edge solutions and services that leverage real-time payments. Incumbents, such as traditional banks and credit unions, will need to modernize their digital footprint to meet customer expectations in this era.

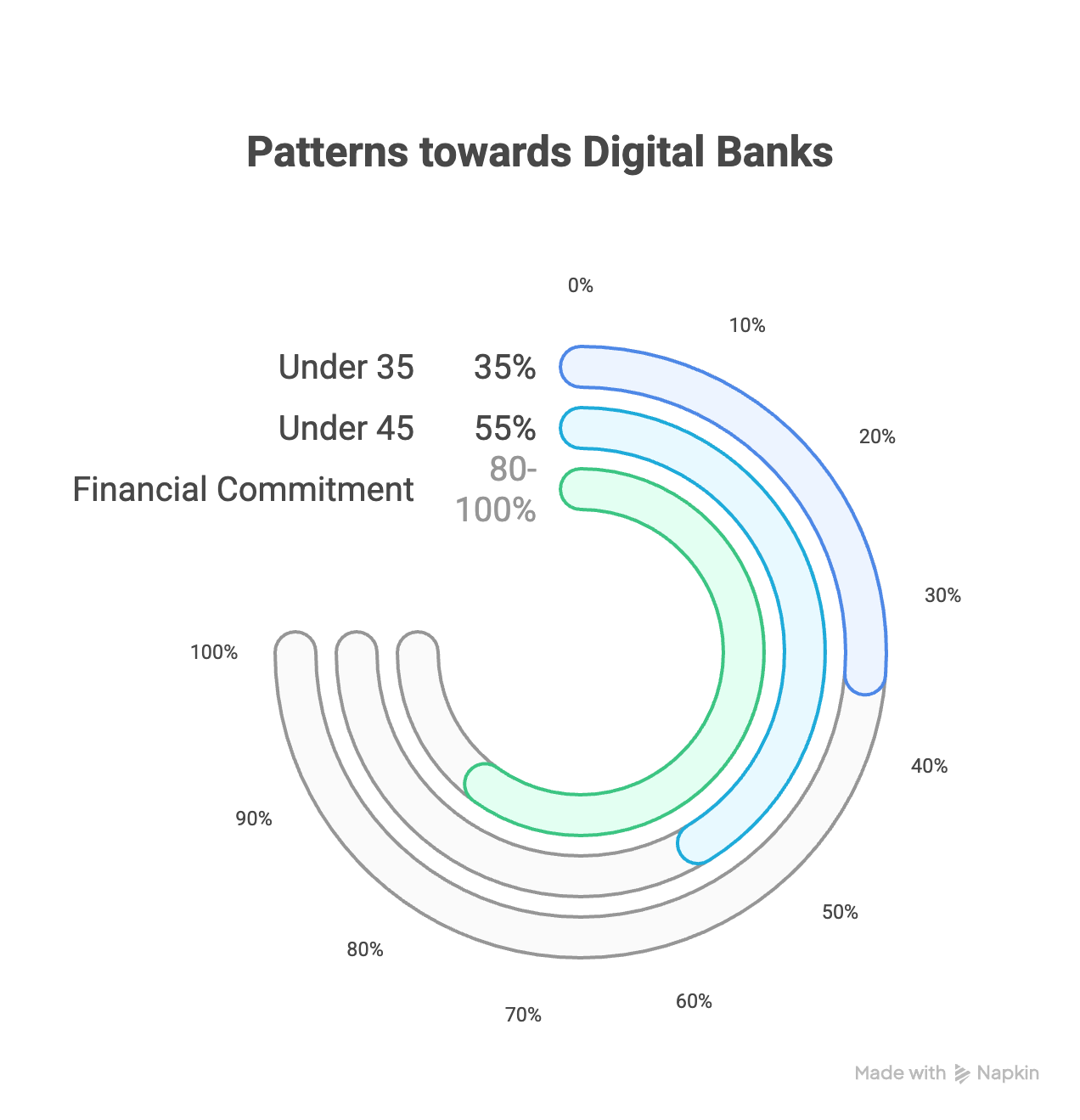

If we look across the Atlantic in Europe where real-time systems are present, younger & tech-savvy customers are gravitating towards digital banking and fintechs, where 35% of primary clients for digital banks are under 35, and over half (55%) are under 45 according to Kearney consultancy. We also see a trend with those that are on these platforms keep 80% to 100% of their finances at these institutions.

If we look at day-to-day banking needs where neobanks and fintechs seem to focus heavily, it accounts for up to 49% of a Bank's revenue (source: McKinsey). Tie that to the fact that the price-to-book ratio for banks globally is 0.9, meaning that markets don't believe banks are generating enough value.

What is RTR and why you should care

RTR is an effort to modernize the national Canadian payment system and is governed under the Canadian Payments Act. Imagine not having to wait several days for payments to go through, for small businesses this could reduce significant overhead for payroll. Perhaps a startup has just secured funds, well those funds would get to them faster than previously. Cash flow management can be just-in-time (borrowing from lean here) improving liquidity.

It's none too soon either, other countries such as UK, Australia, US, and broadly EU countries have similar systems implemented. For Canadian businesses to remain competitive in a global market it becomes a necessity to modernize.

As part of the modernization the underlying infrastructure that powers payments must be upgraded, as it's decades old banking systems. RTR includes components for

real-time exchange, clearing and settlement including for 3rd party exchanges

centralized fraud system

Comprehensive by-laws, rules and standards

RTR is adopting the ISO 20022 messaging standard and that improves the data richness allowing for automated reconciliation. One could, for instance, include pay stub information within the payments now.

Opportunities for Fintechs

Why have I stated this as a benefit for fintech organizations? First, Payments Canada has opened the network for direct participation from Fintechs and Payment Service Providers (PSPs). Many may no longer need to coordinate with a partner bank for the payment component, arguably a prerequisite for open banking.

Fintechs don't have the technical debt that traditional banks have and have lower operating costs as physical presence is less of a concern. The core heart of these systems tends to be the underlying technology that enables these systems. It means these systems are built around integration from the start, they're using modern technology and processes.

Risks for traditional FIs

Banks and credit unions have issues related to long-term technical debt, meaning any realistic transition requires significant effort. There are opportunities to capitalize but given the mid-market is busy with M&A and consolidation of tech stacks, room for innovation is limited.

It's time the investment in architecture, infrastructure, and security matching current requirements or these businesses risk losing to nimbler organizations. A significant portion of the risk lies building capability and resourcing in house, often employees aren't trained on modern tooling and processes which can impede any initiatives in these areas. Even trying to capitalize on partnerships will require modern infrastructure and cybersecurity practices.

While they are still full-service institutions, losing a large chunk of day-to-day banking will mean customers will look for alternative means to their needs.

Planning your rollout

Far too often organizations misalign when planning rollouts. The vision needs to unite business units and emphasize the importance of the new digital model, capabilities means including time for upskilling and supporting teams during the transition phases, and finally systems/tools to adapt to these new workflows.

Cybersecurity becomes a bigger concern

In 2008, when UK launched its real-time payments systems, online banking fraud rose by 132% (source: EY), the landscape has since changed considerably. It's one of the reasons we see an emphasis on central fraud system from Payments Canada.

From an organizational perspective, these kinds of requirements highlight why it's important to move towards automation and industry best practices such as shifting left or simply put catching problems earlier in the development lifecycle. It can be up to 100x cheaper to find these issues earlier, where something that could have been $100 to fix during development can cost $10,000 in production.

Another recommendation for focusing maturity would be looking across 5 pillars for security: identity, devices, network segmentation, applications and workloads, and data. Integrating these into your workflow you will want to:

Verify explicitly using identity, device, location, behavioural analytics

Provide least privilege access so that user's only have what's necessary to do their job

Assume breach and minimize the footprint within your network

Continuous monitoring and analytics to be able to respond to any threats quickly.

Planning Ahead

Real-time Rail (RTR) represents a significant advancement in the Canadian payments system, bringing about faster and more efficient transactions. It offers numerous opportunities for fintech companies to innovate and thrive, while posing considerable challenges for traditional banks and credit unions to modernize their infrastructure and security measures.

As the rollout of RTR progresses, it is essential for organizations to align their vision, upskill their teams, and adopt modern tools and workflows to remain competitive. Cybersecurity will play a critical role in this transformation, highlighting the importance of robust practices and continuous monitoring. Embracing these changes will be key to future-proofing the Canadian financial landscape and meeting evolving customer expectations.