Vote, Trade, Innovate.

What the election means for credit unions on Canada’s Trade Corridor

As the Canadian election draws near, I wanted to dive into what Mark Carney's promise of a Canadian trade corridor would mean for digital innovation and financial services. Countries with similarly remote communities, such as Australia, India, and Kenya, have modernized their digital infrastructures, leading to significant adoption of digital banking—89% and 78% of users respectively by 2021, and in Kenya's case, an 83% increase in digital financial services by 2019.

These advancements translate to real economic value. McKinsey Digital estimated that the core digital sectors in India could double their GDP this year, reaching between $355 to $435 billion. However, such impressive numbers don't come about by chance; they require cooperation between the public and private sectors to develop innovative platforms that benefit citizens.

Today, I want to explore digital innovation opportunities specifically for Credit Unions.

Rural Opportunities

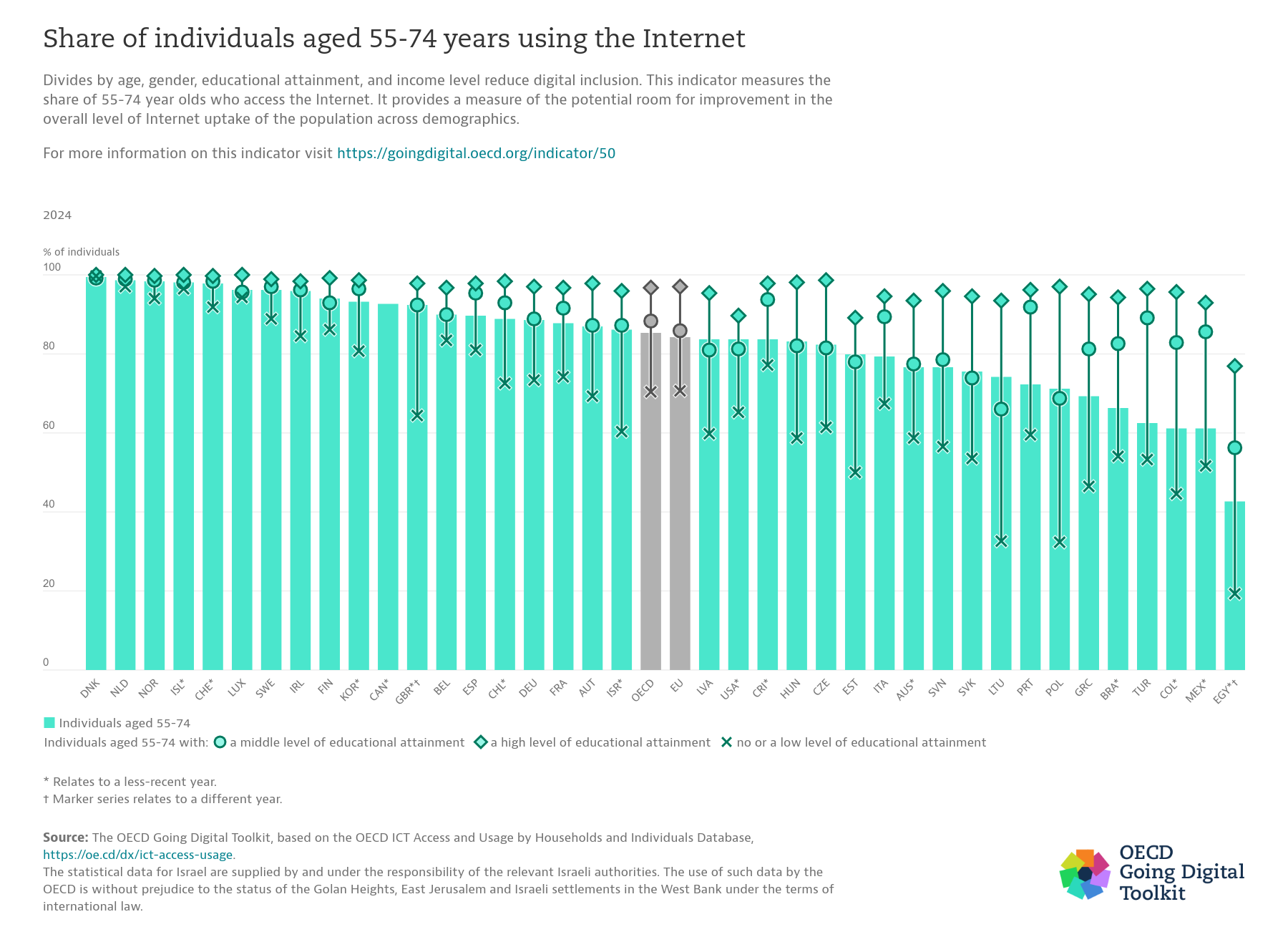

According to Stats Canada (2021), approximately 30% of Canada's GDP comes from rural communities, there is commitment & focus to grow the GDP in these areas. The country's investment through the Universal Broadband Fund aims to enhance high-speed internet access and cellular signals, which will make access to digital systems easier. The corridor will focus on these areas, and they will benefit unequivocally.

Looking at the countries I mentioned above, simply providing access to high-speed internet and cell services is insufficient. There's an opportunity to partner with public sector to push innovative collaboration.

Credit unions have been pursuing mergers to hedge growth and reduce risk; the focus needs to shift to providing modern digital infrastructure which would allow key industries to collaborate on a trade corridor. Canadians as a whole have strong trust in digital services, Credit unions services are significantly behind their counterparts; even with mergers, consolidation of IT isn't enough to provide modern services.

Fintech Collaboration

While it will allow other financial institutions, particularly fintech easier access to these communities, looking at the data credit unions are still imperative. Seniors still have a strong need for physical presence of branches as there is more trust but make no mistake, the trend is toward digital services, and physical footprint alone isn't enough.

Banks are limiting risk by collaborating with fintech businesses, and once they prove their value they are acquired. While credit unions have regulatory requirements for limiting risk and cannot make the same types of plays as banks - there is opportunity for collaboration between credit unions and fintechs that adhere to regulatory requirements. For fintechs that adhere to regulatory requirements, many of them are dependent on other financial institutions for those services which provides a mechanism to integrate as they will have similar underlying tech.

This would require having an architecture that is able to integrate new services quickly. Cloud providers such as Azure can speed time to market with PaaS offerings and building internal architecture to focus on API based services.

As part of this modernization the capability of internal teams needs to be augmented. Fintech tends to hire industry veterans, developers that are the best in their field. While credit unions don't have the same IT budgets, technology is a team support - you can choose to play "Moneyball" (it's a movie worth watching) to build a team that is greater than the sum of its parts and can support modernization efforts.

Opening up collaboration between credit unions

In terms of collaboration between credit unions, most have their tech outsourced heavily. So much so that there are guidelines on risk management associated with outsourcing from OSFI. It means most credit unions are using a handful of systems such as veripark, ebankit, etc. This is an opportunity to build synergies that haven't previously existed.

With inter-provincial mergers going forward, it's easy to see that the financial space is changing. Credit unions looking to support a trade corridor need to be able to support businesses that will be working along these. That means having systems that can communicate across provincial boundaries.

Let's explore some of the benefits of collaborations beyond mergers.

Reduce the cost & risk of innovation - We didn't land on the moon in the first go; there were several failed attempts. Fundamental shifts mean big impacts and these have risks. Collaborating to provide services that are traditionally strengths for credit unions such as local community presence while building a digital footprint

Competing in a changing market - let's face it, a strong digital footprint is necessary for continued growth of credit unions. Rather than compete internally, they should collaborate to compete with larger market forces. The Big Banks have massive budgets and still control roughly 80% of the market, on the other side of the spectrum you have fintech businesses that often go around regulatory requirements - both groups are squeezing in on territory that would traditionally be credit unions. Combining forces to provide a unified digital experience would create a more equal playing field.

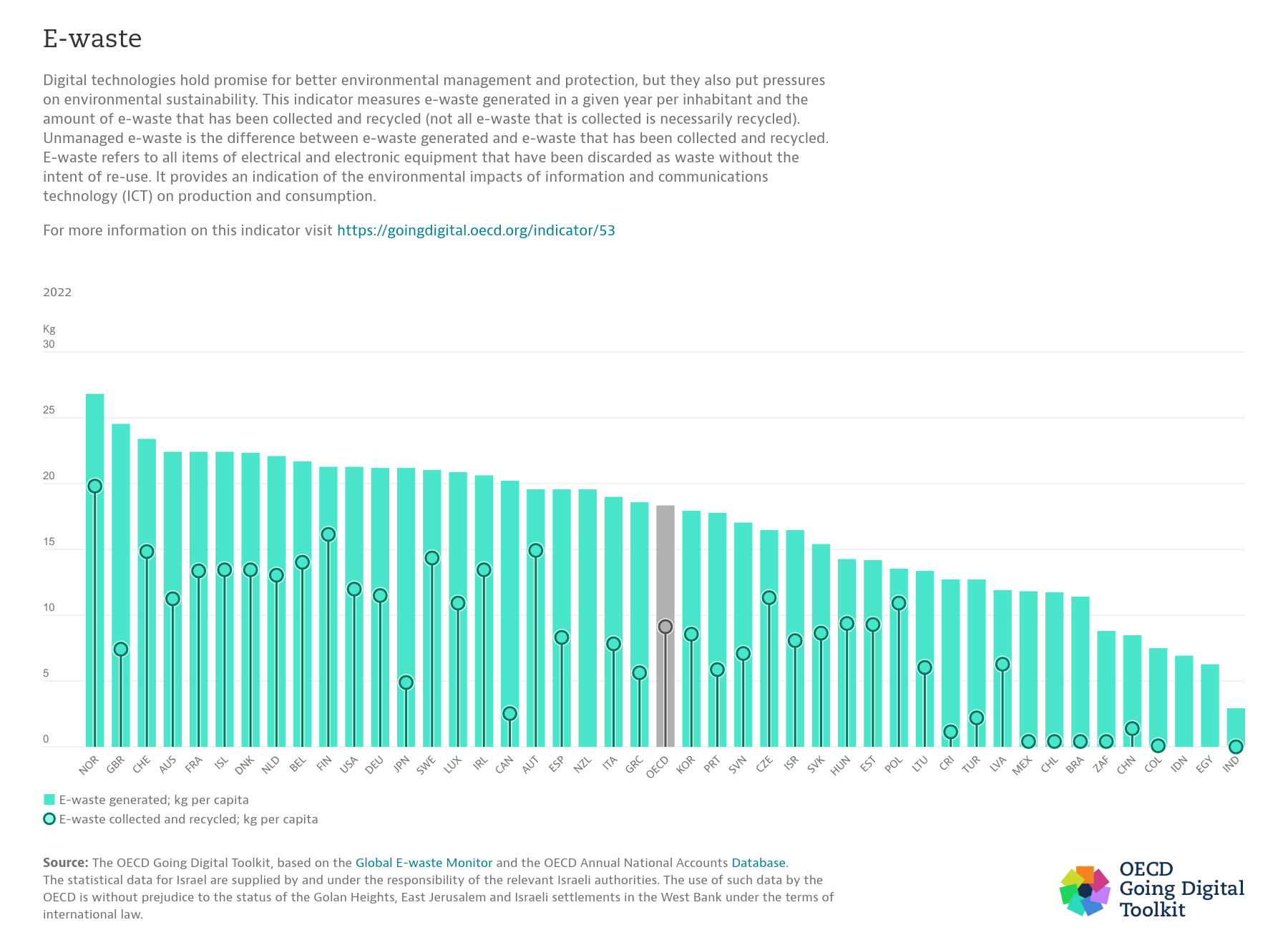

Green Investments

Canada has room to improve in green investments specifically for e-waste. Credit Unions are about local investments, e-waste becomes imperative to manage. Additionally, in our back yard Canada has some of the largest Cleantech innovations happening and the room for investments is massive.

Investing in local e-waste removal systems would be unique to credit unions and an area (particularly sustainability related initiatives) where traditional banks have minimal footprint. In fact, banks such as RBC focus on oil & gas energy businesses.

Tying the need for green investments into the local economy and showing the value added via digital means would increase consumer confidence in the unique value of credit unions. A few projects that come to mind:

We have some of the cheapest & green electricity in the world, large rural areas for data center investments.

Investing in green transportation such as ferries and tying those to smart cities are necessary investments and areas where credit unions could differentiate themselves while sticking to community benefit leaders.

Need for tech

All of these solutions require strong digital systems. I, as someone working with credit unions, wasn't aware of their unique value until I got involved and I suspect most people are in that category. It means being able to show members your value in a real-time digital format. If you can prove to consumers where your investments are going, trust will grow and it will fuel membership growth.

Investing in technology to keep the lights on will no longer be sufficient, and those that do will not succeed in the long run.